2. Economic analysis framework

2.1 Background

A number of existing TBhC appraisals and appraisal procedures were examined during the preparation of this Part of the Guidelines. Key objectives were to investigate what problems had been encountered in applying existing appraisal procedures to TBhC projects, why these procedures were considered unsuitable for TBhC projects and how, if at all, other countries/jurisdictions had overcome these issues. The New Zealand Transport Agency and the United Kingdom Department for Transport in particular have introduced guidelines in this area in recent years.

Perceived problems and issues raised in relation to TBhC appraisals include the following:

- Existing economic analysis guidelines were mainly focused on infrastructure projects or projects that change generalised cost for existing users.

- TBhC projects often do not change the actual service level, quality or price (and hence generalised cost) of any mode.

- Effects are diverse and dispersed and hence difficult (and/or costly) to measure, estimate and incorporate accurately in an appraisal – the effort involved in this is often not justified by the project cost as TBhC projects tend to be smaller projects.

- There is uncertainty and an apparent variability in the diversion rates and other effects (such as lengths and timing of avoided trips).

- Diversity of TBhC projects means that analysts have to adapt existing procedures and cannot just 'follow the formula'.

- Newness of TBhC means analysts have to make assumptions and projections on limited experience, which results in inconsistent treatment of various aspects in appraisals.

The examination of existing TBhC appraisals did not find a common approach on many of these issues. It is apparent that a significant degree of approximating, aggregating and averaging will need to be accepted for most small to medium scale TBhC projects.

Most appraisals attempted to deal with the above problems and issues within a CBA framework. This is appropriate for the following reasons:

- Many of the benefits of TBhC projects are of the same types as those of other projects, such as travel time savings for remaining road users and reduced environmental externalities. Unit values for these benefits already exist. It may be more difficult to estimate the effects/changes to which to apply these unit values in the case of TBhC projects, but this problem is likely to lessen as further post-implementation monitoring and evaluation evidence is accumulated.

- Transport authorities are likely to want to propose TBhC initiatives as part of integrated packages of measures that combine road, public transport and walking/cycling projects, and possibly pricing measures. These packages will be easier to analyse and compare if consistent appraisal procedures have been used for all components and for alternative investments.

- Given that a CBA framework forms the basis of the economic analysis guidelines for other modes, a similar framework for TBhC has the advantage that analysts already have a working knowledge of the framework.

- A further advantage of using a CBA framework for TBhC projects is that if such projects are as effective as some experience to date indicates they may be, the use of appraisal procedures that enable them to be compared directly with other types of transport interventions will help to establish their credibility more quickly with policy and funding agencies.

Based on these considerations, a CBA framework is appropriate for the appraisal of TBhC projects and the guidance in this Part follows the same general principles set out in the ATAP Guidelines for public transport - that is, with:

- Transport system user benefits derived from changes in perceived costs (that is, changes in consumer surplus) and with resource cost corrections added/subtracted to translate the analysis to resource costs

- Costs and benefits discounted to present values to reflect the relative value of impacts in future years

- Indicators such as the benefit–cost ratio (BCR) and net present value (NPV) used to show the economic merit of the initiative.

2.2 Theoretical framework

Travellers make travel decisions based on their perception of their total ‘cost’ of travel, where this cost includes monetary amounts paid (and perceived as being incurred) and a range of other quality and service factors such as the time, comfort, reliability, security and cleanliness of travel.

The ‘cost’ is usually described as the private generalised cost of travel, but may also be called the perceived cost of travel or the behavioural cost of travel. The private generalised cost of travel is used to forecast the mode and route choice of trips. As it represents the perception of users, it also represents their willingness-to-pay for a journey and hence is used to value changes in their travel choices. Refer to the mode specific parts of these Guidelines and Part T2 for further discussion of generalised cost/price.

A key feature and objective of TBhC initiatives is people changing between modes (such as from car to public transport or cycling and walking). When people change modes, they make this decision on the basis of their perception of the relative costs of the alternative modes. Some of these perceived costs are different from resource costs. CBA is based on resource costs, so CBA procedures need to include adjustments (termed resource cost corrections) to offset these differences.

A conventional theoretical framework for CBA of transport projects involving users changing between modes (of which TBhC projects are a subset) assesses the benefits as the sum of the following:

- (A) Benefits of the project to existing users of the 'to' mode[1] (estimated as changes in private generalised cost for that mode, usually including cost, time and comfort aspects)

- (B) Perceived benefits to new users of the 'to' mode, including mode changers (generally valued at half the unit benefits to existing users of the 'to' mode)

- (C) Benefits from avoidance of unperceived costs[2] associated with the 'from' mode (the previous behaviour of mode changers), comprising:

- (i) resource cost corrections for mode changers themselves, including monetary (such as car maintenance and other non-fuel variable vehicle operating costs and car parking costs) and non-monetary (such as accident trauma)

- (ii) other resource cost impacts (externalities) on other transport system users or of the transport system (such as decongestion and reductions in private car-related environmental and accident externalities)

- (D) Unperceived costs associated with the new users of the 'to' mode, comprising:

- (i) resource cost corrections for mode changers themselves, including monetary (such as public transport fare payments that are perceived as a cost but in fact are a transfer rather than a resource cost[3]) and non-monetary (such as health benefits of cycling and walking, which may be under-perceived)

- (ii) other resource cost impacts (externalities) on other transport system users or of the transport system (such as environmental, accident and health externalities - to the extent that the costs of poorer health were being incurred by society rather than the behaviour changer).

Category (A) benefits are the benefits to existing users of the mode that is improved by the infrastructure project or public transport service improvement. Benefits to existing users are changes in generalised cost and usually include mainly aspects of cost, time and comfort.

If people change mode in response to an infrastructure project or public transport service improvement, their perceived benefits (B) are valued at half the unit benefits to existing users (A) (the 'rule of half'). When choosing between modes, travellers are assumed to fully perceive relative time and comfort aspects and out of pocket costs such as fuel, tolls, parking charges and public transport fares. These aspects/costs are taken into account in their choice of mode and are assumed to be included in (A) and (B).

However, travellers’ perceived benefits usually do not equate to all of the resource cost changes resulting from a project, which are necessary for transport project appraisal. For the mode changers, the resource cost adjustments (C(i) and D(i)) are also added. These represent the additional unperceived resource cost savings to the behaviour changers themselves resulting from replacing a car trip with a public transport trip (or cycle/walk trip) that are not included in the perceived (rule of half) benefit.

Finally, the other resource cost impacts on other transport system users or of the transport system (C(ii) and D(ii)) are added. These include decongestion and net environmental externalities.

This is the approach used in appraising public transport initiatives and it is also considered to be the most appropriate framework for economic appraisal of TBhC initiatives. The approach and principles are also similar to those used for evaluating user benefits in situations where there is induced traffic.

2.3 Application of framework to TBhC projects

TBhC programs change the information available to households and individuals and, partly as a result, their perceptions about alternative travel modes and choices – even where there are no changes to the system itself.

Economic theory assumes that decision makers have perfect knowledge about the attributes of the choices available to them. TBhC initiatives start from the premise that people’s knowledge is imperfect and can be improved. The benefit is the same as would occur had the actual range, quality and prices of the choices available to them been improved, when in fact it is only their knowledge of the range, quality and prices of available choices that has improved.

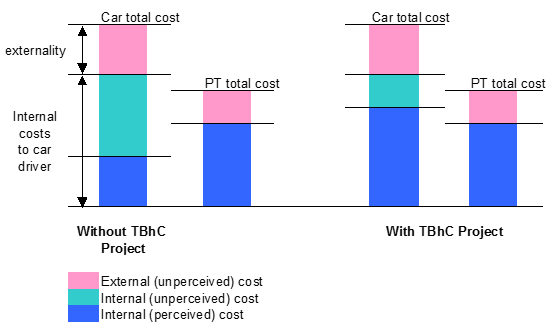

Figure 1 breaks down the costs associated with a car trip into perceived and unperceived components, including externalities. Normally, car drivers only consider the internal perceived costs described above and shown in the blue shaded lower segments in the figure. Other internal costs, such as non-fuel variable vehicle operating costs and accident costs, are considered to be unperceived as shown by the middle green shaded segments (X). Externality costs (such as environmental effects), shown in the top pink shaded segments, are also generally considered to be unperceived.

Figure 1: Categories of costs associated with a car trip

One of the effects of a TBhC project is to provide travellers with information that changes their perceptions of costs of different modes. This is illustrated by the two scenarios on the right hand side of Figure 1. The first scenario shows the situation if the TBhC program corrects a proportion of the internal unperceived costs (X). Segment Y shows remaining unperceived internal costs of the car trip following the TBhC project. This is the required resource cost correction that is counted as a benefit in addition to the net perceived benefit if a car trip is removed by a TBhC project. The second scenario shows the situation where all internal costs are perceived as a result of the TBhC project and the required resource cost correction is reduced to zero. TBhC projects can also induce mode changes by reducing the perceived costs of 'to' modes.

TBhC projects primarily involve 'soft' measures such as marketing and information that aim to change perceptions and knowledge about different travel options and choices rather than changing generalised cost. Therefore category (A) benefits are typically zero or negligible for TBhC projects. Some types of TBhC projects, such as school travel plans, may involve some infrastructure improvements that change generalised cost for people already using that infrastructure, and this may still need to be quantified in some cases if significant. If an initiative will result in significant existing user benefits, the component of the package that is producing these benefits should be assessed separately using the public transport or active transport guidelines.

Also it could be argued that the more accurate perception of costs that is achieved by the TBhC project is a benefit to existing users even if they do not change mode or they already use environmentally friendly modes. This effect is ignored as the TBhC appraisal is mainly interested in actual behaviour change, not simply changed 'travel awareness' without any change in behaviour.

Estimating category (B) benefits is therefore difficult with TBhC projects. Normally, the benefits to mode changers can be valued at half of the unit benefits to existing users (Category A) but, as noted above in the case of TBhC projects, such benefits are often zero. The benefit to mode changers cannot be zero or people would be indifferent about changing behaviour. The explanation, as noted above, is that TBhC programs change households’ and individuals’ perceptions about alternative travel modes and choices even where there are no changes to the system itself.

In the case of TBhC projects, people make changes because the new information:

- Corrects an information gap or misperception and they realise that the alternative actually is more attractive on balance than the private car trip that it replaces

- Changes their attitude so that they are willing to accept the disadvantages of the alternative mode because they feel that it is the right thing to do - for example, they feel they are being more environmentally responsible. This is still a valid benefit.

The change in perceived benefits/disbenefits resulting from the TBhC project causes people to make the travel behaviour change as they now perceive the cost of making the trip by car as being higher than the alternative. This is shown in Figure 2.

Figure 2: Change in perceived costs resulting from TBhC project

In the situation without the TBhC project, Figure 2 shows that for a particular individual the perceived costs of travel by public transport are greater than by car, so car is the preferred mode. The TBhC project causes the individual to become aware of a greater proportion of the actual costs of car travel and, as a result, the perceived costs of a car trip now exceed those of undertaking the trip by public transport and public transport becomes the preferred mode. The difference between the car total resource cost and public transport total resource cost represents the benefit of this behaviour change. Some of this accrues to the behaviour changer as savings in perceived and unperceived internal costs and some to society due to the lower externality costs associated with a public transport trip compared with a car trip. Note that there is no actual change in the total cost of either the car or public transport trip, but that the behaviour change and resulting benefits arise solely from the change in perceived costs brought about by the TBhC project.

In the above example, changes in internal unperceived costs of travel behaviour changers are the category C(i) and D(i) benefits, or resource cost corrections, in the theoretical framework. Category C(i) benefits will include unperceived costs of car use (car maintenance and other non-fuel variable costs, tolls, parking subsidies, part of accident costs, health costs and so on) and D(i) will include public transport fares and cycle costs.

In summary, consistent with the analysis of public transport projects, the economic appraisal of TBhC initiatives involves estimation of the following three main benefit categories:

- User benefits – benefits to travel behaviour changers (the users’ perceived benefits from their changed travel choices)

- Resource cost corrections – changes in the resource costs that are borne by or affect travel behaviour changers but are not perceived by them, and adjustments for transfer payments that are perceived as costs by travellers but do not represent use of any resources

- Externality benefits (disbenefits) – reductions (increases) in resource costs that are neither perceived nor borne by the travel behaviour changer.

These benefit categories are considered in more detail in Section 4.

[1] The 'to' mode is generally the mode that is being improved by the transport project. In the examples given here the 'to' mode is public transport and/or cycling and walking while the 'from' mode is the private car. These would be reversed in the case of a highway improvement.

[2] Unperceived costs comprise all variances between perceived costs and resource costs and include privately incurred resource costs that are not perceived (e.g. most non-fuel private vehicle operating costs), private costs that are perceived but are not actually resource costs (e.g. fares, tolls and fuel taxes), and externalities to third parties (e.g. environment and accident-related externalities).

[3] Any increase in operating costs for the 'to' mode (in this case public transport) are accounted for in full in the costs side of the CBA, yet the fare payments (which are a transfer reflecting this same cost) are included in the perceived net benefit of new users of the 'to' mode (as a disbenefit). A resource cost correction equal to the fare is required to avoid double counting of costs.